Are you ready to grow your business? With the turn of a new year, it’s a great time to take action. And good news…the U.S. Small Business Administration (SBA) actually created the 504 Loan Program to offer business owners a more affordable and accessible way to grow and expand.

The SBA 504 Loan Program is designed to help business owners be successful. Let’s dive in to the top three ways the 504 does this.

Improves Cash Flow

Improved cash flow is of vital interest to all businesses. Business owners faced with high-interest mortgages or upcoming balloon payments can greatly benefit from the SBA 504 Refinance Program. SBA 504 Loans provide access to equity a borrower has built up in real estate while re-amortizing with a low, long-term, fixed interest rate product.

The SBA 504 Refinance Loan is government-backed financing that comes with three huge advantages. One, it offers business owners a below-market, fixed rate and a repayment period of up to 25-years. Two, the down payment requirements are as low as ten percent and are often fulfilled by existing equity in the project. And three, borrowers can elect to get cash out for business expenses. Cash can be taken out for salaries, rent, repairs, maintenance, inventory, utilities, credit cards, lines of credit, etc.

To qualify for refinancing, the mortgage(s) to be refinanced must be at least two years old and originally used for the purchase or improvement of fixed assets. Payment history is important too…no late payments of 30+ days in the past year. Keep in mind…loans that currently have a government guarantee (7a, USDA, 504, etc.) do not qualify for a 504 refinance.

Using the 504 to Refinance Debt…

The 504 Loan is perfect for refinancing existing commercial mortgages when:

- The loan is at least two years old

- The property being refinanced is at least 51% owner occupied or long-term equipment

- The debt to be refinanced was originally used for the purchase or improvement of fixed assets

- The business has been current on the debt to be refinanced for the past 12 months?

Options

- Multiple loans can be consolidated and/or refinanced

- Up to 90% loan-to-value (first and second combined)

- Cash out available up to 85%

- FIXED for 20 or 25 years on 504 loan

Controls Overhead Costs

Entrepreneurs typically start their business in a leased facility. In fact, many small business owners think financing a commercial real estate purchase isn’t even an option because they fear the down payment requirements will be too high. However, buying or constructing a new facility with 504 provides a great opportunity for fixing occupancy costs and locking in low interest rates. Other benefits include:

- Builds equity: each payment is an investment in the future

- Occupancy costs are stabilized: rent increases no longer apply and the SBA 504 payment is fixed

- Preserves cash: in most cases, with the 504, the monthly payment to own is less than a rent payment

By locking in a low rate, which is fully amortized for up to 25 years, borrowers see predictable monthly payments. Plus, 504 Loans have no future balloon payments.

SBA 504 loans also allow borrowers to roll closing costs, soft costs, and other fees into the loan, thus preserving cash. Not to mention, the cost of equipment, furniture and fixtures, parking lots, architectural fees, etc. can also be rolled into the loan.

Using the 504 to Finance Commercial Real Estate…

The 504 Loan is perfect for:

- Purchasing land

- Purchasing existing facilities

- Construction of new facilities

- Modernizing, renovating or converting existing facilities

Streamlines or Increases Production

Whether the business is product or service based, having the necessary equipment is vital to maintaining smooth operations. However, replacing, upgrading, or purchasing new equipment can put a serious pinch on cash flow. A 504 Loan offers business owners a more affordable way to get needed equipment without making a substantial dent in the bottom line.

504 Loans are perfect for the purchase and installation of new or used, fixed, long-life machinery and equipment, such as:

- X-Ray or Digital Imaging Machines

- Manufacturing Equipment

- Dry-Cleaning Equipment

- Commercial Printers

- Food Processing Machinery

- Highly Calibrated Machines

- Equipment that generates renewable energy

Using the 504 to Finance New Equipment…

The 504 Loan is perfect for the purchase and installation of new or used, fixed, long-life machinery and equipment, such as:

- X-Ray or Digital Imaging Machines

- Manufacturing Equipment

- Dry-Cleaning Equipment

- Commercial Printers

- Food Processing Machinery

- Highly Calibrated Machines

- Equipment that generates renewable energy

Options

Whether you’re just replacing a piece of existing equipment or buying a larger facility and stocking it with all new equipment, the SBA 504 has flexible financing options.

- Machinery and equipment can be financed independent of real estate or in conjunction with a commercial real estate purchase.

- Or, machinery and equipment can be financed in conjunction with a commercial real estate purchase

- Loan terms of 10-, 20- or 25-years are available (term length is limited to the useful life declaration provided by the manufacturer)

Practical Examples of How Businesses Use SBA 504 Loans

Working capital was hard to come by…

A local retail provider was seeking working capital to purchase inventory and pay business expenses. Since the business owned its commercial real estate, the lender suggested a 504 Refinance Loan. The 504 allowed the borrower access to the equity they’d built in the real estate while re-amortizing with a low, long-term, fixed interest rate product. With a lower interest rate and better terms, the retailer lowered their monthly payment and accessed much needed working capital without taking on additional debt.

A balloon payment was looming…

A manufacturing company was four years into their mortgage payments and business was booming. However, with a five-year term loan, the balloon payment was quickly approaching. The lender stepped in and offered a recommendation for refinancing with the SBA 504 Program’s Refinance Loan…a long-term financing option with low fixed interest rates. This allowed the client to stabilize their expenses and spread their predictable payments out over 25 years.

A stalled expansion got back on track…

A wholesale bakery, nearing the end of a lease term, received news their business property was being sold and needed vacated. Facing an inevitable move, the business owner decided to make the most of the situation and began to seek a property that would not only house the business but would also allow for expanded production.

Nearby land was purchased, and construction of a larger building began. However, due to cost overruns, conventional financing could no longer allow for the completion of the construction…the borrower suddenly required a higher advance rate than the bank could offer. Exploring alternative options in hopes of getting the expansion back on track, the lender suggested the 504 Loan Program and they found it to be the perfect solution.

The participation of the 504 Loan Program allowed the bank to offer a 90% advance, which gave the business the financing they needed to pay contractors and finish the project. The new location offers ample space to produce, distribute and sell an expanded line of bakery items.

New Opportunities to Grow Your Business: Think 504 When…

- You are looking to buy, build or renovate a commercial facility

- You need to finance the purchase of heavy machinery or equipment

- You are looking to add multiple retail locations

- Your business is buying real estate as part of a business acquisition

- An owner wants to sell his/her share of real estate to the other owners

- A balloon payment is coming due on your commercial mortgage and you want to refinance the debt into a long-term, fixed-rate loan

- A 25-year loan could help manage your operating capital

12 benefits that prove SBA 504 Loans were specifically designed to help businesses expand and prosper…

SBA 504 Loans from Growth Corp feature:

- Low down payments (10% in most cases)

- Low, fixed interest rate on the 504 portion

- Long loan terms (10-, 20-, or 25-year terms)

- The ability to include furniture, fixtures and fees

- An option for refinancing commercial debt

- Payment stability

- Preservation of working capital

- Protection from balloon payments

- The ability to include leasehold improvements

- Up to $5 million for SBA portion of the loan, and no limit on the overall project size

- The option of using the 504 Loan Program multiple times to continue expansion

- The ability to keep your current bank/lender

How Does the 504 Loan Program Work?

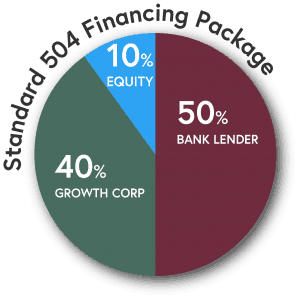

The 504 program offers financing that covers 90% of a project’s total cost, as opposed to the 70%-80% offered with most conventional loan programs. The typical breakdown of the funds in a 504 loan is:

The 504 program offers financing that covers 90% of a project’s total cost, as opposed to the 70%-80% offered with most conventional loan programs. The typical breakdown of the funds in a 504 loan is:

- 50 percent from a bank or other private lender,

- 40 percent from the SBA, and

- 10 percent from the borrower

Business owners can reduce their initial capital outlays by as much as $1 million in some circumstances by leveraging the 504 Program’s 90 percent loan-to-cost financing.

To qualify for the SBA 504 Loan Program, the business must:

- have fewer than 500 employees

- be located in the United States

- be a for-profit business

- have a tangible net worth of not more than $15 million and average net income after taxes (two years prior to application) of not more than $5 million

- be owner-occupied

- if a manufacturing company, meet the definition of a small to mid-sized manufacturer as classified in the North American Industry Classification System, sectors 31-33.

Keep in mind…SBA 504 Loans are offered in conjunction with local banks, not in competition with them!

Why Growth Corp?

We know your success depends on having access to expansion capital. We offer affordable and accessible expansion capital to grow your business. Our experienced staff takes pride in making a difference in the lives of small business owners and their employees. Start-ups to seasoned businesses and everything in between can benefit from working with Growth Corp. Here’s why:

- We’re the #1 SBA 504 Lender in Chicago and Illinois. Growth Corp also consistently ranks as one of the top ten SBA 504 Lenders nationwide.

- SBA recognized Growth Corp as an Accredited Lender after a thorough review of its policies, procedures and prior performance. The prestigious ALP status grants Growth Corp increased authority to process and close 504 loans, which provides expedited processing of loan approvals and closings.

- We simplify the loan approval process. Our team coordinates the entire process from application through closing, funding and servicing, making it seamless for you and your bank lender.

- We are SBA 504 Experts. Our responsive and educated staff focuses almost exclusively on SBA 504 loans. We’ve got the process down to a science!

- We’ve worked with thousands of businesses, spanning various industries. That means, there’s not much we haven’t seen. Your goals, project structure and business type will likely be familiar to us and we’ll understand your unique situation.

- Our mission is to advocate for small business. We love our communities and believe small business is the foundation of their economic prosperity. We will do all we can to support you and your business goals.

If you run a small to medium sized business in and need financing to purchase machinery/equipment or construct/purchase a new building, Growth Corp’s team of professionals will work with you directly to provide the best financing strategy for reaching your goal. Contact any member of our Lending Team today!