Let’s check out some examples of how businesses use the SBA 504 Refinance Program to unlock additional capital and secure low, fixed interest rates on financing, amortized over 20 years, for up to 90% of the appraised value of the commercial real estate property. In addition, we’ll look at how borrowers can also take cash out for qualified business expenses such as salaries, rent, utilities, inventory, etc.

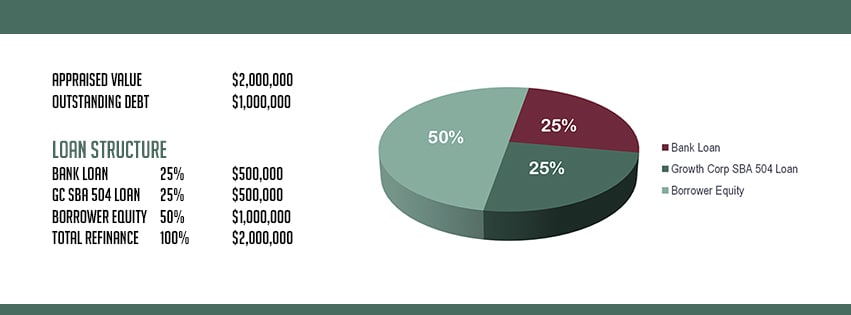

EXAMPLE 1: Refinancing a Conventional Loan

- A borrower seeks to refinance an existing $1 million commercial real estate loan.

- The property appraises at $2 million.

- An acceptable structure would be:

Comments:

The new third party loan must be equal to or greater than the SBA 504 debenture amount, at least $500,000 in this example.

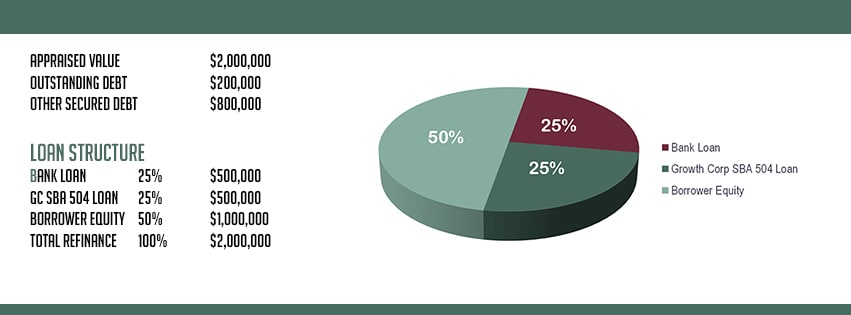

Example 2: Refinancing Multiple Conventional Loans

- Borrower seeks to refinance an existing $200,000 commercial mortgage plus, an $800,000 second mortgage borrowed five years ago for 504 eligible business purposes

- Property appraises at $2 million

- An acceptable loan structure could be:

Comments:

Both the original first mortgage and the existing second mortgage can be combined. The new third-party loan must be equal to or greater than the SBA 504 debenture amount, at least $500,000 in this example.

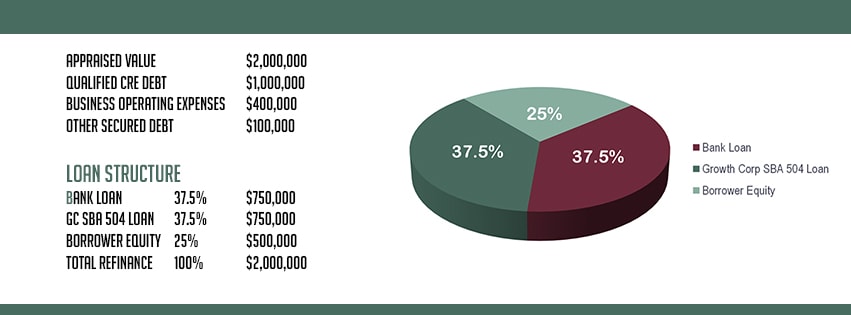

Example 3: Cash Out for Eligible Business Expenses

- Borrower seeks to refinance $1 million in existing qualified commercial real estate debt, plus $400,000 borrowed three years ago for equipment and inventory, plus $100,000 to serve as next year’s salary for a new employee

- Property appraises at $2 million

- An acceptable loan structure could be:

Comments:

The Refinance Program can be used for both restructuring qualified debt and accessing equity for business operating expenses. Because the LTV amount does not exceed 85% and business operating expenses do not exceed 25% of the appraised value, this request meets SBA Refinance Program guidelines.

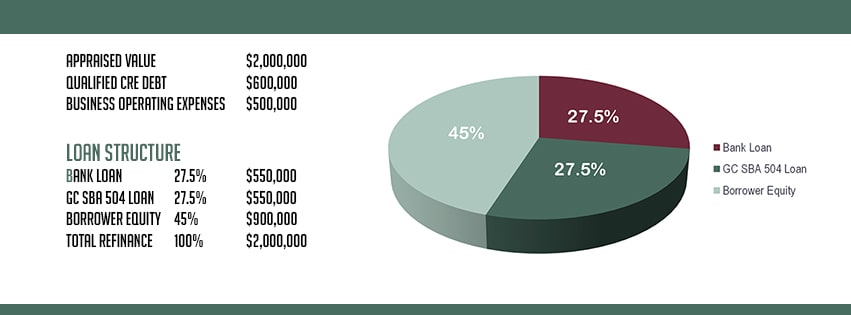

Example 4: Cash Out for Eligible Business Expenses

- Borrower seeks to refinance $600,000 in existing qualified commercial real estate debt, plus $800,000 for unsecured loan obligations and business operating expenses

- Property appraises at $2 million

- An acceptable loan structure could be:

Comments:

The Refinance Program can be used for both restructuring qualified debt and accessing equity for business operating expenses. While the total refinance request does not exceed 85% LTV, only $500,000 of the $800,000 requested can be included because the total amount for operating expenses cannot exceed 25% of the appraised value.

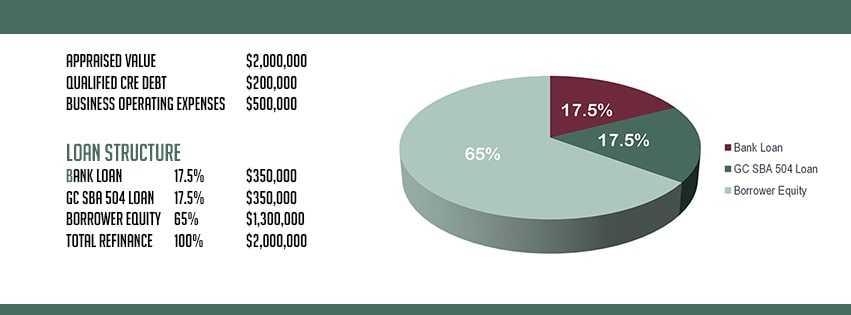

Example 5: Cash Out for Eligible Business Expenses

- Borrower seeks to refinance $200,000 in existing qualified commercial real estate debt, plus $1.3 million for business operating expenses, some of which will be incurred in the next six months

- Property appraises at $2 million

- An acceptable loan structure could be:

Comments:

The Refinance Program can be used for both restructuring qualified debt and accessing equity for business operating expenses. While the total refinance request does not exceed 85% LTV, only $500,000 of the $1.3 million requested can be included because the total amount for operating expenses cannot exceed 25% of the appraised value.