SBA 504 Loan Chicago: How to buy commercial real estate with 10% down

If you are a Chicago-area business owner paying rent on commercial space, you may be closer to owning that building than you think.

The SBA 504 loan is one of the most powerful financing tools available to small businesses, and it is widely underused, especially in the Chicago market. With as little as 10% down, eligible businesses can purchase, build, or renovate owner-occupied commercial real estate and lock in a below-market fixed rate for up to 25 years.

This post breaks down exactly how it works, who qualifies, and how to get started.

What Is an SBA 504 Loan?

The SBA 504 loan is a government-backed financing program administered through the U.S. Small Business Administration. It is specifically designed to help for-profit businesses purchase major fixed assets, primarily owner-occupied commercial real estate and long-term equipment.

The SBA 504 loan is a government-backed financing program administered through the U.S. Small Business Administration. It is specifically designed to help for-profit businesses purchase major fixed assets, primarily owner-occupied commercial real estate and long-term equipment.

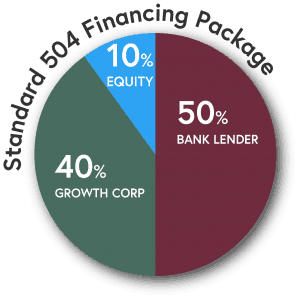

Unlike conventional commercial loans, the 504 program uses a three-party structure:

- 50% or more: Provided by a bank or conventional lender

- Up to 40%: Provided by a Certified Development Company (CDC), backed 100% by the SBA

- As little as 10%: Your equity injection (down payment)

That structure is what makes 10% down possible. And because the CDC portion carries a long-term fixed rate, your monthly payments stay predictable for the life of the loan.

Why Chicago Business Owners Use the SBA 504 Loan

Chicago is a competitive commercial real estate market. Industrial space in the suburbs, retail storefronts in neighborhood corridors, and professional office suites near the Loop all carry significant price tags.

Conventional commercial loans typically require 20% to 30% down, plus variable rates that can climb over time. For many small businesses, that down payment alone is a dealbreaker.

The SBA 504 loan changes that math.

Key benefits for Chicago businesses:

- 10% down on most eligible projects, preserving capital for operations, hiring, and growth

- Fixed rate on the CDC portion for 10, 20, or 25 years, with no balloon payment

- No limit on total project size (the SBA debenture portion maxes at $5 million, or $5.5 million for manufacturers and certain public policy projects)

- Closing costs can be rolled in, further reducing out-of-pocket expenses

- Fully amortizing structure, meaning you are building equity from day one

For business owners tired of rent increases and lease uncertainty, the 504 is often the most direct path to ownership.

How the Loan Structure Works: A Chicago Example

Say a Chicago-area professional services firm wants to purchase a $2 million commercial building.

Here is how a typical SBA 504 structure looks:

| Source | Percentage | Amount |

| Bank / Conventional Lender | 50% | $1,000,000 |

| CDC (SBA 504 Debenture) | 40% | $800,000 |

| Business Owner (Down Payment) | 10% | $200,000 |

| Total Project Cost | 100% | $2,000,000 |

The bank portion carries the lender’s own terms. The CDC portion carries a long-term fixed rate. The business owner puts in $200,000 instead of the $400,000 to $600,000 a conventional lender might require.

That preserved capital stays in the business.

What Properties Qualify in Chicago?

The SBA 504 loan is for owner-occupied commercial real estate. The business must occupy at least 51% of the property (60% for new construction).

Eligible property types in the Chicago area include:

- Office buildings and professional suites

- Retail storefronts and service businesses

- Industrial, warehouse, and manufacturing facilities

- Medical and dental offices

- Mixed-use buildings (where the business occupies the required percentage)

Investment properties and speculative real estate purchases do not qualify. The property must be used in the operation of your business.

Who Qualifies for an SBA 504 Loan in Chicago?

Basic eligibility requirements include:

- For-profit business operating in the United States

- Net worth under $20 million and average net income under $6.5 million (after taxes) over the past two years

- Business use: The financed asset must be owner-occupied and used in the operation of your business

- Creditworthy: Demonstrated ability to repay from business cash flow

- No federal loan defaults

Startups and special-use properties (gas stations, car washes, hotels, etc.) typically require 20% down rather than 10%.

Businesses do not need to be headquartered in Chicago specifically. Growth Corp serves all of Illinois, including Cook County, DuPage, Lake, Will, Kane, and the broader Chicagoland area.

What CRE Agents Should Know

If you work in commercial real estate in Chicago, understanding the SBA 504 loan makes you a stronger advisor to your business-owner clients.

Here is what matters for deal structure:

- 10% down opens the buyer pool. Clients who cannot swing a conventional 20-30% down payment may still qualify for a 504.

- Eligible uses include acquisition, renovation, and new construction. Ground-up builds and major improvements to existing properties both qualify.

- The 504 can be combined with an SBA 7(a) loan for projects that include both real estate and working capital components (subject to current SBA policy).

- Closing timelines vary but are generally comparable to conventional commercial closings when working with an experienced CDC.

- The CDC relationship matters. Growth Corp has closed thousands of SBA 504 transactions across Illinois. We know how to move deals to close.

Bringing a CDC into a conversation early can be the difference between a deal that dies at financing and one that closes.

The SBA 504 Process: Step by Step

Step 1: Pre-qualification Talk to a CDC like Growth Corp to review your project, your business financials, and your goals. This conversation is free and takes less than 30 minutes.

Step 2: Lender introduction Growth Corp works with banks and conventional lenders across Chicago to structure the full financing package. We can introduce you to lenders who know the 504 program.

Step 3: Application and underwriting You submit your financials, the property details, and supporting documents. Growth Corp handles the CDC portion of the underwriting and SBA submission.

Step 4: SBA approval The SBA reviews and approves the debenture. Growth Corp manages this process on your behalf.

Step 5: Closing Both the bank loan and the CDC debenture close. You bring your 10% equity injection. The deal funds.

Step 6: You own your building.

Frequently Asked Questions

Can I use an SBA 504 loan to buy a building in Chicago? Yes. Eligible businesses that will occupy at least 51% of the property can use an SBA 504 loan to purchase owner-occupied commercial real estate anywhere in Illinois, including Chicago and the surrounding suburbs.

What is the minimum down payment for an SBA 504 loan? Most eligible businesses put down 10%. Startups (in business less than two years) and special-use properties typically require an extra 5%, or in the case of a project being for a start-up and special-use property, the down payment would be 20%.

Is there a maximum loan amount? There is no cap on total project size. The SBA debenture (CDC) portion is capped at $5 million for most projects, or $5.5 million for manufacturers and certain public policy projects. The bank portion can be larger.

How long does it take to close an SBA 504 loan? Timelines vary based on the complexity of the deal and how quickly documents are gathered. Working with an experienced CDC like Growth Corp helps keep the process on track.

Can a CRE agent refer a client to Growth Corp? Absolutely. We work with commercial real estate professionals across Illinois. Reach out through growthcorp.com and we will connect your client with the right lending team member.

What if my business is a startup? Startups (less than two years in operation) can still qualify but will typically need 15% down rather than 10%.

Ready to Take the Next Step?

Growth Corp is Illinois’s leading SBA 504 lender, ranked #8 in the country by loan volume with a portfolio over $1 billion. We have helped businesses across Chicago and all of Illinois stop renting and start owning.

If you are a business owner exploring your options, or a CRE agent with a client who needs creative financing, we want to talk.

Visit growthcorp.com or reach out to our lending team directly.

- Chicago / Northern Illinois / Iowa: Joel Herscher, Steve Kirby, Ryan O’Neill

- Central / Southern Illinois / Missouri: Nick Kern

The SBA 504 loan is one of the best-kept secrets in commercial real estate finance. For Chicago businesses, it is also one of the most practical paths to long-term ownership.

Let’s build something together.

Growth Corp is a Certified Development Company authorized by the U.S. Small Business Administration to administer the SBA 504 Loan Program. All loans subject to SBA eligibility requirements and approval.