With the celebration of Earth Day upon us, are you ready to go green? The U.S. Small Business Administration (SBA) and U.S. Department of Energy (DOE) are teaming up on a shared mission: to inspire entrepreneurs and small business owners to leverage SBA loan programs for making improvements in energy efficiency. These agencies are helping small businesses improve and modernize their buildings, save on utility costs and, ultimately, increase their bottom line.

Going Green Can Help You Save Green

If you’d like to go green, SBA’s 504 Green Loan Program offers special incentives for incorporating energy efficiency or renewable energy into building projects. The 504 Green Loan Program is designed to assist small businesses with financing real estate and equipment purchases. The loans are generally used for large projects that will make a positive impact on their community through job creation and local economic development. Here’s what’s eligible:

- Reduce energy use by at least 10% Improvements to a building currently occupied by the borrower must show a minimum of 10% reduction to energy usage (compared to historical consumption) through upgrades in equipment such as improved lighting, insulation, HVAC and other energy consuming equipment. Borrowers purchasing or constructing a replacement property must be relocating to a similar region (as determined by SBA) with potential for similar historical energy consumption.

- Generate at least 15% renewable energy The property must have upgrades performed that produce at least 15% renewable energy. Energy that can be produced includes solar, wind, geothermal, hydropower, and biomass.

- LEED Certification* If historical energy consumption records for the property are not available, a project can qualify if it is built or retrofitted using LEED certification standards through the completion of upgrades.

*Maximum SBA/CDC contribution $5.5 million per project

More Green Energy, More Money

The SBA 504 Green Loan program is a financing option that presents an incentive for small businesses to increase their building’s sustainability through energy efficiency and/or renewable energy solutions. The program offers up to $5 million in financing per project and can receive a maximum of $16.5 million in aggregate funding. The funding can be increased to $5.5 million if public policy goals are met and can be used for multiple SBA 2nd mortgages. Loans can also be used to purchase land (including existing buildings), improve company assets, begin new construction projects, and renovate or upgrade existing buildings. So, by spending less on your utilities, you can actually get more capital for your business improvement project!

Breakdown of Key Benefits:

- Larger SBA/CDC Loan Amount – SBA maximum contribution increases to a $5.5 million cap with no maximum total project limit.

- Higher Option for Aggregated Lending – Borrowers can have multiple SBA 504 Green Project loans with $16.5M aggregate cap limit on capital (up to the maximum SBA/CDC contribution of $5.5 million per project).

- Save Money – Reduction in energy costs will have long-term financial benefits for the business, while most energy improvements/equipment can be financed within the loan.

The Benefits of Going Green

Increased loan limits and utility bills savings aren’t the only benefits of going green. Investing in energy efficiency can also:

- Reduce operating costs – by saving on operation and maintenance costs with longer-lasting, more efficient lighting

- Improve the building’s air quality – by reducing air leakages and drafts and increasing the amount of daylight

- Enhance your brand image – by increasing the value of your asset to potential renters and marketing to environmentally concerned customers

How the 504 Loan Program Offers Additional Help with Going Green

Besides the typical benefits of 504 Loans, which include low, fixed rates, long loan terms (up to 25 years) and low down payments, the 504’s Green Initiative adds the following benefits:

- Up to $5.5 million per project

- Removes the dollar limit on the SBA portion

- Slashes the banks’ risk to 50% of the project costs

- Allows borrowers to take multiple loans

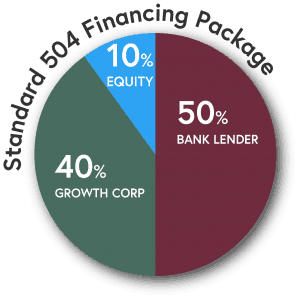

SBA 504 Loan Structure

Typical structures for the 504 Loan Program involve a partnership between a non-profit CDC (such as Growth Corp), a participating bank, credit union or other lending institution and the borrower.

- 40% of the total project cost is provided by a non-profit CDC

- 50% of the total project cost is provided by a participating lender (typically a bank)

- 10% of the total project cost is provided by the applicant small business borrower

How to Qualify

Below are the four main qualifications the SBA requires for you to qualify for a green loan.

- Be a for-profit company

- Be 51% or more owner-occupied

- Have a tangible net worth of less than $15 million

- Have an average net income after federal income taxes (excluding any carry-over losses) from the preceding two completed fiscal years of $5 million or less.

With the down economy, should I wait to make capital improvements?

Not at all. In fact, use of the 504 Loan Program has become increasingly important as a source of long-term financing since traditional sources of money have declined in recent months. The program was designed to provide small businesses access to capital that might not otherwise be available through conventional means.

About the SBA 504 Loan Program

The SBA 504 Loan Program is an economic development tool that provides small businesses with long-term, fixed rate loans to help them acquire major fixed assets for expansion or modernization of their businesses. These loans are most frequently used to acquire land, buildings, machinery or equipment. A 504 loan can be a 10-, 20- or 25-year term, which is beneficial for small business owners. Pairing the fixed rate aspect with these term lengths gives small business owners stability, allowing them to budget and manage cash flow without concerns about rising rates or balloon payments.

About Growth Corp

Small Business Growth Corporation (Growth Corp) is a nonprofit, mission-based lender dedicated exclusively to connecting small businesses with quality expansion capital through administration of the SBA 504 Loan Program. With a commitment to economic development, job creation and the small business sector, Growth Corp is ranked a Top 10 National CDC for SBA 504 loan volume and is Illinois’ largest 504 loan provider. In fact, Growth Corp’s substantial portfolio ($740+ million) is particularly impressive because every dollar was utilized by Midwest entrepreneurs to open and expand their small businesses. Contact any member of our lending team today!