How to Apply for SBA 504 Loan Illinois: Step-by-Step

If you’re a business owner in Illinois looking to purchase real estate, expand operations, or invest in major equipment, the SBA 504 loan program can be one of the most powerful financing tools available. With below-market, fixed interest rates and long repayment terms, it’s designed to help small businesses grow without straining cash flow.

In this step-by-step guide, we’ll walk you through exactly how to apply for SBA 504 loan Illinois and how Growth Corp can help you navigate the process from start to finish.

What Is an SBA 504 Loan?

The SBA 504 loan program is a government-backed financing option that helps small businesses fund major fixed assets like:

- Commercial real estate (purchase, construction, or renovation)

- Large equipment or machinery

- Long-term business expansion projects

A typical SBA 504 loan structure includes:

- 50% from a traditional lender (bank or credit union)

- 40% from a Certified Development Company (CDC) like Growth Corp

- 10% from the borrower

This structure reduces risk for lenders and makes it easier for businesses to secure affordable financing.

Who Qualifies to Apply for SBA 504 Loan Illinois?

Before applying, it’s important to make sure your business meets the basic eligibility requirements:

- Operates as a for-profit business in the U.S.

- Has a tangible net worth under $20 million

- Has an average net income under $6.5 million (after taxes)

- Uses the funds for eligible fixed assets

- Occupies at least 51% of the property being financed

Ineligible uses include:

- Working capital or inventory

- Speculative real estate investment

- Refinancing existing debt (with limited exceptions)

Working with a trusted Illinois CDC like Growth Corp ensures you meet all SBA requirements before moving forward.

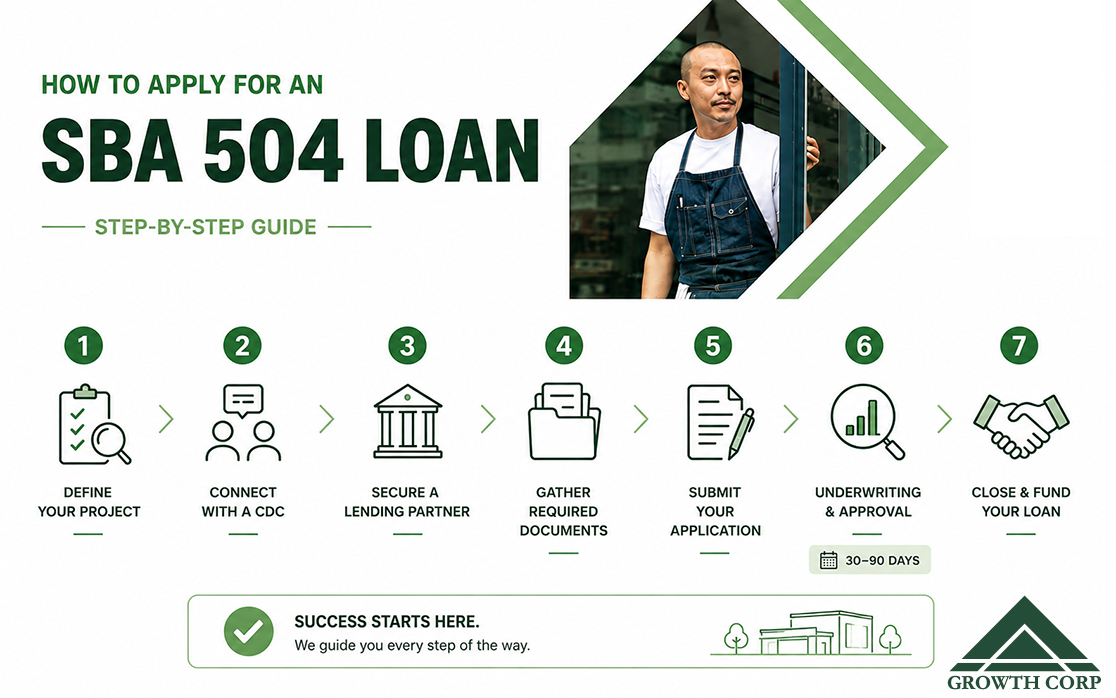

Step-by-Step: How to Apply for SBA 504 Loan Illinois

Step 1: Define Your Project

Start by outlining exactly how you plan to use the loan. This might include:

- Purchasing a building

- Constructing a new facility

- Renovating an existing space

- Buying long-term equipment

Having a clear project scope will help determine your loan amount and eligibility.

Key questions to ask yourself:

- Will my business occupy at least 51% of the building?

- Is this a long-term, fixed-asset purchase?

- Is my business for-profit and based in Illinois or our service territory?

Step 2: Connect with a Certified Development Company (CDC)

A CDC like Growth Corp is your key partner in the SBA 504 process. Growth Corp originates and services the SBA 504 portion of the loan for businesses throughout Illinois and select counties in Iowa, Indiana, Kentucky, and Missouri.

We:

- Guide you through eligibility requirements

- Structure your financing package

- Work directly with your lender and the SBA

Getting in touch early can save you time and streamline the process.

Step 3: Secure a Lending Partner

You’ll need a bank or credit union to fund 50% of the project. If you already have a banking relationship, talk to your commercial lender first and ask them to partner with Growth Corp on the SBA portion. If you do not have a lender yet, Growth Corp works with a broad network of Illinois banks and can help you connect.

Step 4: Gather Required Documentation

Once you are moving forward, you will need to compile financial and business documentation. Getting organized early speeds up the process significantly.

Typical documents required:

- Three years of business tax returns

- Three years of personal tax returns (all owners with 20%+ ownership)

- Current year-to-date profit and loss statement

- Current balance sheet

- Personal financial statement for each owner

- Business debt schedule

- Purchase contract or construction estimates for the project

- Business license and formation documents

Step 5: Submit Your Application

Your CDC (Growth Corp) will guide you through the SBA application. This includes:

- Completing SBA Form 1244 (the 504 application)

- Submitting all required financial documentation

- Providing a business plan if required

- Signing applicable certifications and disclosures

Your CDC will compile and submit your SBA 504 loan application. Growth Corp works closely with both you and your lender to ensure everything is accurate and complete before submission.

Step 6: Underwriting and Approval

Both the bank and Growth Corp will underwrite your loan independently. The SBA reviews and approves the CDC portion.

What happens during underwriting:

- Credit review of the business and owners

- Cash flow and debt service analysis

- Property appraisal (for real estate projects)

- Environmental review (if required)

- Title search

Timeline varies but typically ranges from 30 to 90 days depending on project complexity and how quickly documentation is submitted.

Step 7: Close and Fund Your Loan

Once both loans are approved, you will close on the bank portion, and the SBA 504 debenture is funded shortly after. For real estate purchases, the transaction closes like a standard commercial real estate deal.

After approval:

- Your bank funds its portion

- The CDC funds the SBA-backed portion

- You contribute your equity

Growth Corp coordinates the SBA closing process and stays with you through funding.

Why Work with Growth Corp in Illinois?

Choosing the right CDC can make or break your experience with the SBA 504 program. We are ranked #8 nationally by SBA 504 loan volume and manage a portfolio of over $1 billion. Growth Corp has deep experience helping Illinois businesses secure financing with:

- Local expertise and statewide reach

- Personalized, hands-on guidance

- Strong relationships with lenders

- A streamlined, efficient application process

We’re committed to helping businesses grow through smart, accessible financing solutions. Whether you are buying your first commercial building or expanding an existing facility, we help you move from application to closing with clarity at every step.

We work with businesses across all of Illinois and select counties in neighboring states. Our team includes regional loan officers who know Illinois markets and lender relationships well.

Ready to apply for SBA 504 loan Illinois financing? Contact any member of our team to discuss your project.

Frequently Asked Questions

How long does an SBA 504 loan take to close in Illinois? Most loans close within 60 to 90 days from application, depending on project complexity and how quickly all documentation is submitted.

Can I use an SBA 504 loan to refinance my building? In some cases, yes. The SBA 504 debt refinance program allows qualifying businesses to refinance existing commercial real estate debt. Contact Growth Corp to review your specific situation.

Does Growth Corp serve all of Illinois? Yes. Growth Corp serves all 102 Illinois counties, plus select counties in Iowa, Indiana, Kentucky, and Missouri.

What credit score do I need? The SBA does not publish a minimum credit score for the 504 program, but most lenders look for a score of 680 or higher. Strong business cash flow can offset credit considerations in some cases.

Is there a maximum loan amount? The SBA portion is generally capped at $5.5 million (or $5.5 million per project for eligible manufacturers and energy-related projects). There is no hard cap on the bank portion.