You’re Paying Someone Else’s Mortgage. Here’s How to Stop.

If you’re looking at an SBA 504 loan in Illinois, you already know the feeling…

You’ve been in that space for years. You know every quirk of the building, every neighbor in the strip center, every parking problem on a busy Friday. And every month, you write a rent check that builds zero equity for your business.

In 2026, with commercial lease rates still elevated across Illinois and landlords increasingly unwilling to lock in long-term rates, that check is getting bigger while your control over the space gets smaller.

There’s a better path. And it starts with understanding one program most Illinois business owners have heard of but never fully explored: the SBA 504 loan.

The Problem: You’re Building Wealth for Someone Else

Renting is not always the wrong choice. But for an established business with steady cash flow, paying rent on owner-occupied space is often the most expensive long-term financial decision you can make.

Consider what you’re giving up:

- No equity accumulation. Every rent payment disappears.

- No control over your occupancy costs. Lease renewals bring surprises.

- No asset on your balance sheet. Your real estate is your landlord’s retirement plan, not yours.

- No protection from displacement. A lease non-renewal can upend everything you’ve built.

Illinois commercial lease rates have remained stubbornly high coming out of the post-pandemic reset. In Chicago’s collar counties and key downstate markets like Peoria and Rockford, industrial and office rents have stabilized at elevated levels. That means the gap between what you’re paying to rent and what you could pay to own is narrower than it has been in years.

The Solution: SBA 504 – The Loan Illinois Businesses Use to Buy Commercial Property

The SBA 504 loan was designed for exactly this situation. It gives established small businesses a government-backed path to purchase the building they already operate in, or a new facility to grow into.

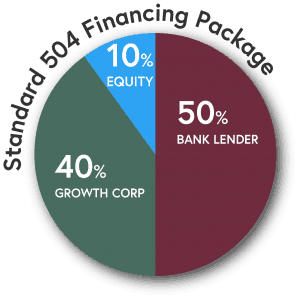

Here is how the structure works:

- Your bank provides 50% of the project cost as a first mortgage.

- Growth Corp, as your Certified Development Company, provides 40% through a 100% SBA-guaranteed debenture.

- You contribute just 10% as a down payment.

That 10% down is the headline. But the real story is what comes with it.

Why an SBA 504 Loan in Illinois Stands Out in 2026

Current SBA 504 rates as of April 2026 sit in the mid-5% range for 20- and 25-year terms. That is a below-market, fully fixed rate, locked for the life of the loan. While conventional commercial real estate loans often carry variable rates tied to prime (currently 6.75%), your 504 rate does not move.

That fixed rate matters more right now than it has in years. With the Federal Reserve signaling continued uncertainty and Treasury yields climbing in early 2026, locking in a fixed rate on a long-term commercial mortgage is a strategic decision, not just a financial one.

Additional benefits of the SBA 504 for Illinois business owners:

- Terms of 10, 20, or 25 years, keeping monthly payments manageable.

- Financing up to 90% of total project costs.

- Eligible for new construction, acquisition, or renovation of owner-occupied property.

- Can include soft costs such as appraisals, environmental reports, and title fees.

Who Qualifies?

You do not need to be a large company. SBA 504 eligibility is designed for Main Street businesses. You generally need to:

- Operate as a for-profit business in the United States.

- Have a tangible net worth under $20 million.

- Have an average net income under $6.5 million after federal taxes for the prior two years.

- Plan to occupy at least 51% of the building you are purchasing (or 60% for new construction).

Sectors that frequently use the 504 in Illinois include manufacturing, healthcare, professional services, childcare, and warehousing. If you are running an established business and paying rent, it is worth a conversation.

Why Growth Corp

Growth Corp is the #1 SBA 504 lender in Illinois and consistently ranks among the top ten CDCs in the country. We have helped thousands of Illinois business owners stop renting and start owning, from Springfield to Chicago to Rockford and every market in between.

We know the Illinois commercial real estate market. We know the 504 program inside and out. And we move fast, because you should not have to wait months to find out if you can own your building.

Talk to a member of our lending team today at growthcorp.com/about-growth-corp/lending-team. There is no pressure, no jargon, just a straight conversation about whether the SBA 504 makes sense for your business.