SBA 504 Loan Commercial Real Estate Loan: The Complete 2026 Guide for Small Business Owners

If you’re a business owner thinking about buying commercial real estate, expanding operations, or upgrading equipment, there’s a good chance you’ve heard about the SBA 504 loan program. And in Illinois, demand for SBA 504 financing continues to grow because it offers what many traditional commercial loans do not: low down payments, long-term fixed rates, and predictable monthly payments.

For many businesses, an SBA 504 Loan Illinois can be the difference between continuing to lease space and finally owning a building that builds long-term equity.

In this complete 2026 guide, we’ll walk through how the SBA 504 program works, who qualifies, what it can be used for, how the process works in Illinois, and why so many business owners are turning to this financing option to support long-term growth.

What is an SBA 504 Loan?

An SBA 504 loan is a commercial financing program backed by the U.S. Small Business Administration (SBA). It is specifically designed to help small businesses purchase fixed assets such as:

- Commercial real estate

- Owner-occupied buildings

- Heavy machinery and equipment

- Facility renovations

- New construction projects

Unlike a traditional commercial mortgage, the SBA 504 program uses a unique financing structure that reduces the borrower’s upfront cash requirement while offering long-term fixed interest rates.

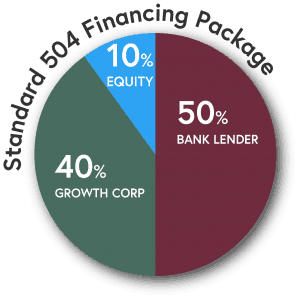

In most cases, the structure looks like this:

- 50% financed by a conventional lender

- 40% financed through the SBA 504 loan

- 10% borrower down payment

That lower equity injection is one of the biggest reasons Illinois business owners choose the program.

What Can an SBA 504 Commercial Real Estate Loan Be Used For:

- Stop Paying Rent: Instead of building equity for a landlord, business owners can invest in property they own. Over time, ownership can strengthen balance sheets and create long-term asset value.

- Preserve Working Capital: Traditional commercial loans often require 20% to 30% down. SBA 504 loans typically require only 10% down for eligible borrowers, allowing businesses to preserve cash for hiring, inventory, marketing, or operations.

- Lock In Long-Term Fixed Rates: The SBA portion of the loan offers fixed interest rates for 10, 20, or 25 years, helping businesses avoid uncertainty from future rate increases.

- Finance Large Projects: The SBA 504 program can support substantial projects involving real estate acquisition, renovations, construction, or equipment purchases.

How the SBA 504 Commercial Real Estate Loan Structure Works

One of the most misunderstood parts of the SBA 504 program is the “two-loan structure.” But once explained, it becomes fairly straightforward.

A typical SBA 504 Loan Illinois project includes:

- The Bank Loan (First Mortgage): A conventional lender finances approximately 50% of the total project cost.

- The SBA 504 Loan (Second Mortgage): A Certified Development Company (CDC), such as Growth Corp, finances approximately 40% through the SBA-backed portion of the project.

- Borrower Equity: The borrower contributes approximately 10% down, although some projects may require more depending on business history or property type.

Business owners typically make separate payments for the bank loan and the SBA loan.

SBA 504 Loan: Rates and Terms in 2026

The CDC portion of your SBA 504 loan carries a fixed interest rate for the full term of the loan. That rate is tied to U.S. Treasury debenture auctions and is set at funding, not at application.

Loan Terms Available

- 10-year term

- 20-year term

- 25-year term (for real estate acquisition)

Rates are inclusive of CDC, SBA, and central service fees. This year, manufacturing businesses (NAICS sectors 31, 32, and 33) receive rates approximately 25 basis points lower due to a waiver of the annual service fee.

For current monthly rate pricing, visit growthcorp.com/sba-504-rate-pricing.

SBA 504 is Designed to Help Businesses Grow

The SBA 504 program is designed for long-term fixed assets that help businesses grow.

Eligible uses include:

- Purchasing owner-occupied commercial real estate

- Building a new facility

- Expanding an existing location

- Renovating commercial property

- Purchasing heavy equipment or machinery

- Refinancing certain commercial real estate debt

- Improving parking lots, landscaping, signage, and site infrastructure

The program is not intended for working capital, inventory, or speculative real estate investing.

SBA 504 Loan Illinois Eligibility Requirements

While every project is unique, most Illinois businesses pursuing SBA 504 financing should expect the following general requirements:

- For-Profit Business: The business must operate as a for-profit entity within the United States.

- Owner-Occupied Property: For existing buildings, the business generally must occupy at least 51% of the property. For new construction, occupancy requirements are typically higher.

- Demonstrated Ability to Repay: Lenders will evaluate business cash flow, historical financial performance, tax returns, debt obligations, management experience

- Good Credit and Financial Standing: Strong credit and responsible financial management improve approval chances, although SBA programs are often more flexible than conventional financing.

SBA 504 vs SBA 7(a): Which Is Better?

The answer depends on your goals.

SBA 504 Loans Are Typically Better For:

- Commercial real estate purchases

- Long-term fixed-rate financing

- Equipment purchases

- Lower monthly payment stability

SBA 7(a) Loans Are Typically Better For:

- Working capital

- Business acquisitions

- Inventory

- Flexible business expenses

- Shorter-term financing needs

Many Illinois business owners choose the SBA 504 program when the primary objective is purchasing real estate with predictable long-term payments.

How Long Does the SBA 504 Process Take?

Every project timeline varies, but many SBA 504 loans take several weeks to a few months from application to funding.

The timeline depends on:

- Project complexity

- Appraisal timing

- Environmental reviews

- Financial documentation

- Construction considerations

- Coordination between lenders and CDCs

- Preparation matters. Businesses with organized financials and clear project plans generally move through the process more efficiently.

Common Questions About SBA 504 Commercial Real Estate Loans

Why do Illinois Business Owners Use SBA 504 Loans? Commercial real estate prices and lease costs continue to pressure small businesses throughout Illinois. Many owners are discovering that purchasing property can create more financial stability than continuing to rent indefinitely.

Can Startups Qualify? Yes, although startups may face higher equity injection requirements or additional underwriting considerations.

Can I Refinance Existing Commercial Real Estate Debt? In some situations, yes. The SBA 504 refinance program can help businesses refinance eligible owner-occupied commercial real estate debt.

Are There Prepayment Penalties? The SBA portion of the loan may include declining prepayment penalties during the first ten years (or seven for a 10-year term) of the loan term.

Can I Lease Part of My Building? Yes, partial leasing is generally permitted as long as occupancy requirements are met.

Why does SBA 504 Lending Continue to Grow in Illinois? Illinois businesses continue to pursue SBA 504 financing because it aligns with long-term ownership and growth strategies. The combination of:

- lower down payments

- fixed interest rates

- extended repayment terms

- commercial real estate ownership creates a compelling financing option in today’s market.

SBA 504 lending volume remains strong nationwide, with thousands of loans supporting small business expansion projects every year.

Final Thoughts

For Illinois business owners looking to purchase property, expand operations, or invest in long-term growth, the SBA 504 program remains one of the most powerful financing tools available.

An SBA 504 Loan can help preserve working capital, stabilize occupancy costs, and position a business for long-term success through ownership instead of leasing.

Whether you are purchasing your first building, constructing a new facility, or refinancing existing commercial debt, understanding how the SBA 504 program works is the first step toward making a more informed financing decision.

If you’re considering an SBA 504 loan in Illinois, working with an experienced CDC and lending team can help simplify the process and determine whether the program is the right fit for your business goals.

Why Growth Corp

Growth Corp is the #1 SBA 504 lender in Illinois and consistently ranks among the top ten CDCs in the country. We have helped thousands of Illinois business owners stop renting and start owning, from Springfield to Chicago to Rockford and every market in between.

We know the Illinois commercial real estate market. We know the 504 program inside and out. And we move fast, because you should not have to wait months to find out if you can own your building.

Talk to a member of our lending team today at growthcorp.com/about-growth-corp/lending-team. There is no pressure, no jargon, just a straight conversation about whether the SBA 504 makes sense for your business.