New lower fees for SBA 504 loan in Fiscal Year 2024 apply to loans approved October 1, 2023, through September 30, 2024, and include a lower annual service fee and the continuation of 0% upfront guaranty fee.

New lower fees for SBA 504 loan in Fiscal Year 2024 apply to loans approved October 1, 2023, through September 30, 2024, and include a lower annual service fee and the continuation of 0% upfront guaranty fee.

SBA 504 Loans

The SBA 504 Loan Program is designed to help business owners be successful. Funds can be used for purchasing land, purchasing existing buildings and construction/improvements (including grading, utilities, parking lots, landscaping, equipment or furniture/fixtures). However, what people might not realize is that the 504 can also be used for refinancing as well.

There is plenty of money available for lending. In fact, the SBA has recently displayed significant effort in making the 504 Loan Program available to even more businesses. With higher loan limits, expanded eligibility standards, and a new debt refinance option, more businesses are now able to utilize the 504 than ever before.

Through the 504 Loan Program, banks can offer long-term financing to small business customers who might not otherwise be able to obtain the necessary financing to grow.

SBA 504 Loan Fees for Fiscal Year 2024

On September 26, 2023, SBA announced the fees for 504 Loans approved October 1, 2023 through September 30, 2024. The fee changes are as follows:

- The upfront guaranty fee remains at 0% at 0.00% in FY24

- The annual service fee decreased from 0.4405% in FY23 to 0.364% in FY24

- For 504 refinance loans, the annual service fee decreased from 0.4559% in FY23 to 0.0.389% in FY24

Check out the 504 Loan Program’s interest rate history. Or, check out what an estimated payment might look like for your business.

For full details read: sba_info_notice_5000-849342_

Almost All For-Profit Businesses Qualify

The 504 Loan Program is a financing tool for economic growth and development that provides small to medium sized businesses with long-term, fixed rate loans to help them acquire major fixed assets for expansion or modernization. These loans are most frequently used to acquire land, buildings, machinery or equipment.

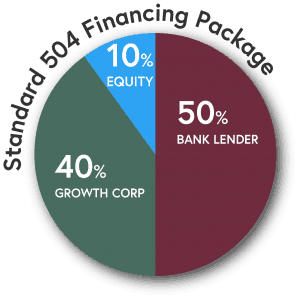

The loan itself is a partnership between you, your CDC (such as Growth Corp), and a local bank. The breakdown typically looks like this:

50% of the project’s total cost will come from a conventional lender (your bank). You and your lender will determine the conditions of that loan, including the amount. This loan is the first mortgage.

50% of the project’s total cost will come from a conventional lender (your bank). You and your lender will determine the conditions of that loan, including the amount. This loan is the first mortgage.- 40% of the project’s total cost will come from a CDC (Growth Corp) with a 10-year or 20-year fixed rate loan guaranteed by SBA. This loan is the second mortgage.

- The remaining 10% of the project’s total cost will come from you, the borrower. Certain types of facilities are classified as “single-purpose” facilities and may require additional equity, but most projects fall into the 50-40-10 split.

50% of the project’s total cost will come from a conventional lender (your bank). You and your lender will determine the conditions of that loan, including the amount. This loan is the first mortgage.

50% of the project’s total cost will come from a conventional lender (your bank). You and your lender will determine the conditions of that loan, including the amount. This loan is the first mortgage.

Medical/Professional

Whether you’re just opening your own practice, or are ready to open a second, third or even tenth office, we’re here to help. We’ve worked with thousands of professionals just like you and we understand the expenses that go into purchasing and furnishing high-end professional offices. Many different types of professionals utilize the 504, such as:

- Doctor’s Offices

- Veterinarian Offices

- Dentists

- Attorneys

- Accountants

- Chiropractors

- Architects

- Graphic Designers

- Physical Therapists

Service Providers

From small, specialty stores to state-of-the-art health clubs, we’ve worked with them all and we understand the nuances and cyclical nature of the service and retail industry. Your number one focus is on your customers and you don’t have time for a lot of paperwork. We get it. That’s why we’ve handled the process for thousands of service providers, such as:

- Restaurants

- Retail Stores

- Health Clubs

- Day Care Facilities

- Car Washes

- Farmers Markets

- Boutiques

- Auto Repair Shops

- Convenience Stores

Manufacturing and Industrial

Whether you need to purchase a piece of highly specialized equipment, are expanding to a larger facility, or are looking to make energy efficiency improvements, we’re here to help you. We’ve been providing financing to manufacturing and industrial firms since 1989 on projects ranging from $200,000 to $20 million, such as:

- Recycling Facilities

- Food Manufacturing

- Steel Production

- Packaging Companies

- Commercial Printers

- Machine Shops

- Freight and Transport

- Wholesalers

Non-Typical or Special Use

Agribusiness Projects

- Grain Elevators

- Irrigation Equipment

- Warehousing and Processing Facilities

- Operations and Fertilizer Plants

- Livestock Feedlots

- Dairy Farm Start-up and expansion

- Livestock Arenas

- Hog Farrow-to-Finish Facilities

Care Providers:

- Assisted Living Facilities

- Independent Living

- Nursing Homes

- Alzheimer’s Facilities

- Drug and Alcohol Centers

- Rehab Facilities

Passive-Income Properties:

- RV Parks

- Campgrounds

- Marinas

- Mini Storage Facilities

Special-Purpose Properties:

- Bowling Alleys

- Medical or Health Facilities

- Sports Arenas

- Wineries

- Auto-Repair Centers

- Car Washes

- Funeral Homes

Other, Lesser-Known Uses of the 504 Loan Program:

- Trucking Company Depots

- Green Initiatives such as Energy Reduction or Renewable Energy

12 benefits that prove SBA 504 Loans were specifically designed to help businesses expand and prosper

SBA 504 Loans from Growth Corp feature:

- Low down payments (10% in most cases)

- Low, fixed interest rate on the 504 portion

- Long loan terms

- The ability to include furniture, fixtures and fees

- An option for refinancing commercial debt

- Payment stability

- Preservation of working capital

- Protection from balloon payments

- The ability to include leasehold improvements

- Up to $5 million for SBA portion of the loan, and no limit on the overall project size

- The option of using the 504 Loan Program multiple times to continue expansion

- The ability to keep your current bank/lender

By and large, use of the 504 Loan Program provides a financing solution that can ease business owners’ expansion concerns. And, with the lower fees in place for FY2024, the 504 is now more affordable than ever before. For more information about who is a good candidate for SBA 504 Loans, download our guide: Typical Users of SBA 504 Loans or contact any member of our Lending Team.