Every year, the U.S. Small Business Administration (SBA) helps Americans secure billions of dollars in financing so they can start or grow a business. However, we still hear some common myths associated with SBA 504 loans. While some are harmless misunderstandings, others can cause business owners to forgo the option entirely. That’s why it’s helpful to get the facts right on the 504 Loan Program so you can make an informed decision on what will work for you.

Myth #1: Successful businesses don’t need an SBA 504 loan.

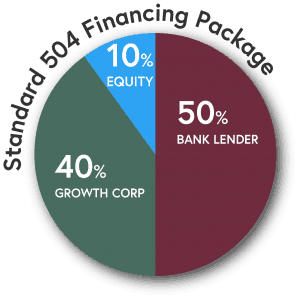

FACT: Many successful small business owners use SBA loans because these loans can offer more flexibility than conventional financing. Benefits include:

- Longer repayment terms – up to 25 years

- Low, fixed interest rates

- Lower down payments

- Flexible repayment options

- The ability to include furniture, fixtures and fees

- An option for refinancing commercial mortgage debt

- Payment stability

- Protection from balloon payments

- The ability to include leasehold improvements

- Preservation of working capital

Myth #2: 504 Loans can only be paid off twice per year.

FACT: A 504 loan can be paid off any month throughout the calendar year, but the calculation is based on the semi-annual debenture dates. Payoff amount includes the remaining principal, prepayment premium (if still applicable) and interest/servicing fees due through the next upcoming debenture date.

- The payoff window for any given month opens on the 2nd Thursday and closes on the 3rd Thursday

- Semi-annual debenture dates are determined by the funding date (i.e. if a loan funds in January, the debenture dates are January 1st and July 1st, February funder – February 1st and August 1st, etc.)

- In order to meet the debenture date, the 504 loan must be paid off the month prior (i.e. for a February 1st debenture date, the loan must be paid off in the January cycle). Please note: if a debenture date is missed, the borrower will incur six months of interest and servicing fees

Myth 3: SBA is a direct lender.

FACT: SBA works with local financial institutions to guarantee a portion of its small business loans and is not, generally, a direct lender. With a federal promise to recoup some of the losses if a borrower can’t make loan payments, financial institutions lend to SBA borrowers with greater confidence. Of course, this guarantee from the SBA only applies to borrowers and financiers that meet its qualifications and approval process.

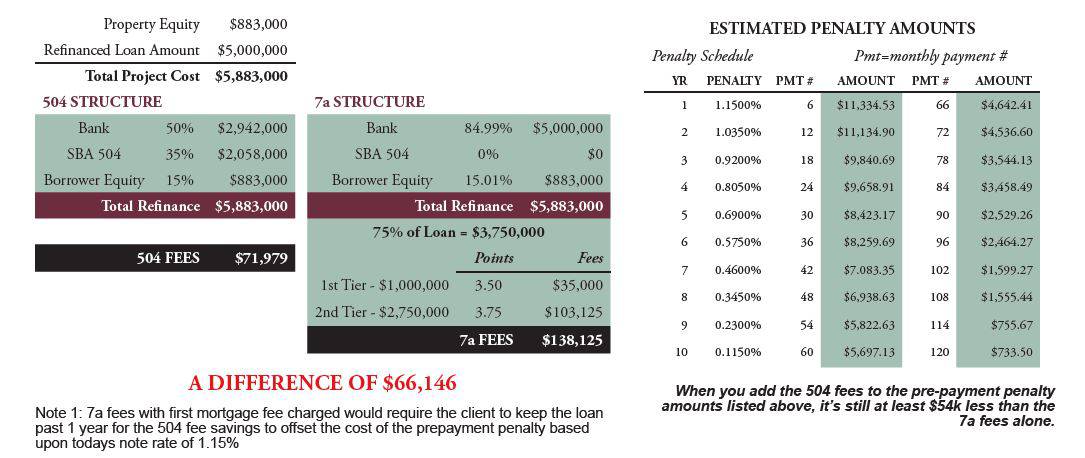

Myth 4: The pre-payment penalties are too high with a 504 loan.

FACT: The prepayment penalty declines in an accelerated fashion over the first 10 years and is eliminated in year 11. And, because there are lower fees associated with 504 loans, the 504 is oftentimes the more affordable choice. The graphic below shows a comparison to the SBA 7(a) program:

Feel free to download our guide: Addressing Myths Associated with the 504

Myth 5: SBA 504 Loans are only for small “mom and pop” businesses.

FACT: The 504 can actually accommodate Middle Market lending quite well. Businesses with a net worth of less than $15 million and a two-year average after tax net income of less than $5 million will qualify for the 504 Loan Program. And, with the 504, there is no cap on the amount of the first mortgage loan provided by the lender. The cap on the 504 second mortgage is a generous $5 million ($5.5 million for manufacturing and green-energy projects). The benefits for middle-market businesses include:

- Capital Preservation

- Below-Market Interest Rates

- Longer Loan Amortization

- Less Impact on Cash Flow

- Reduction in Real Estate Expenses

- Financing can Include Closing and Other Soft Costs

- No Future Balloon Payments

- Predictable Monthly Payments

- Long-Term Fixed Rates

- Large Loan Caps

Want to Learn More?

It’s clear that some small businesses and their advisors rule out the SBA 504 Loan Program because of commonly-held misconceptions. However, these businesses are missing out on the best financing option for owner-occupied real estate and equipment purchases. Or, for refinancing qualified commercial mortgage debt. Contact our team of qualified lenders, who are experts at helping small business owners get approved for SBA 504 loans that can help them compete, grow and succeed.